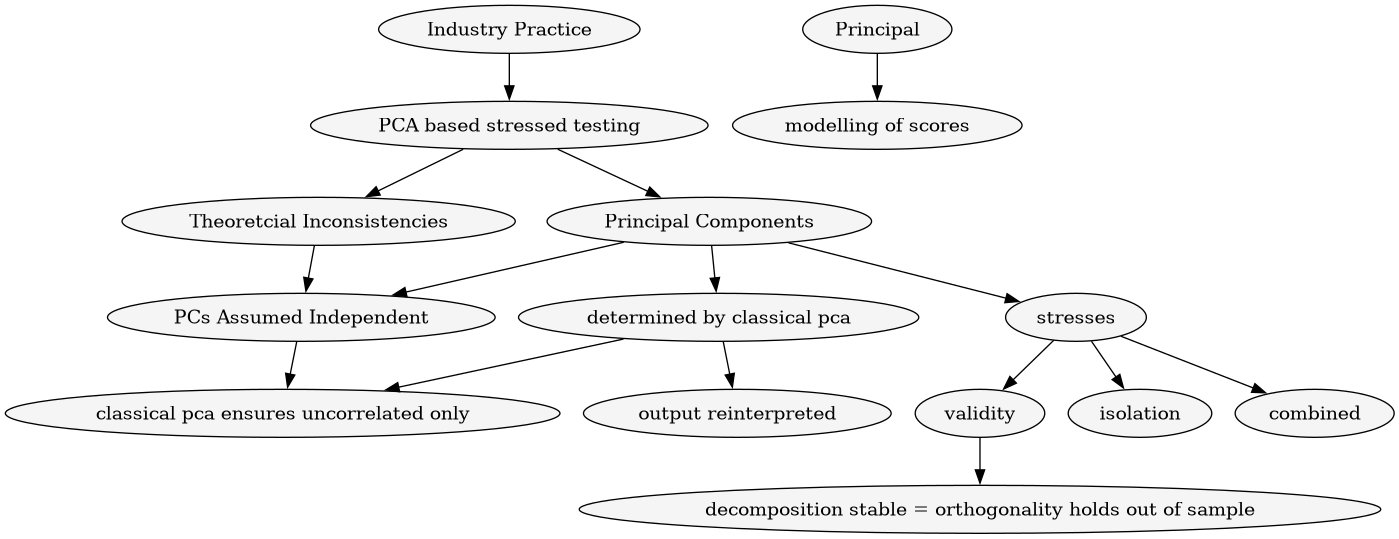

Industry Practice - PCA based stress testing

Life industry typically takes classical PCA , treats the principal components as independent risk factors and stresses them in isolation or combined. ?? , which is only valid if the PCA decomposition is stable and the orthogonality assumption holds out-of-sample. ?? the output of PCA is reinterpreted as a set of orthogonal economic strss scenarios scaled to regulatory confidence intervals

theoretical inconsistencies in industry practice

treating principal components as statistically independent

firstly we treat principal components as independent when stressing them when theoretically they are only uncorrelated and approximately independent and not statistically independent.

?? what part does the gaussian assumption feed into independent component assumption ??

non gaussian modelling of components

an argument for ICA

- data in non gaussian

- we are going to model as non-Gaussian

- we want components that are genuinely independent for scenario generation

under these conditions ICA becomes more theoretically correct tool

a word on the use of copulas by insurers

insurers can go down 2 routes: * independence assumption * or copula for joint behaviour

separating dependence structure from marginal behaviour

copula captures tail dependence that independence assumption misses

Summary

questions

- "fitting marginals that implicitly encode a higher order structure"